MAS Notice 626 runs to 40 pages. Most non-residents who bank in Singapore have never read it. Most articles about Singapore banking compliance paraphrase it in two paragraphs. Neither approach tells you what actually matters: which specific provisions Singapore bank compliance officers apply to non-resident files, how they apply them in practice rather than on paper, and where the gap between regulatory text and bank behaviour creates friction — or, occasionally, opportunity.

I work with both Swiss and Singapore institutions on behalf of non-resident HNWI clients. The compliance cultures differ — Swiss banks run toward precision and formal process, Singapore banks toward risk tiering and pragmatic assessment — but the outcome of a well-prepared file versus an incomplete one is consistent across both systems. Here is what Singapore banks are actually checking on non-resident compliance files in 2026, based on practice rather than policy text.

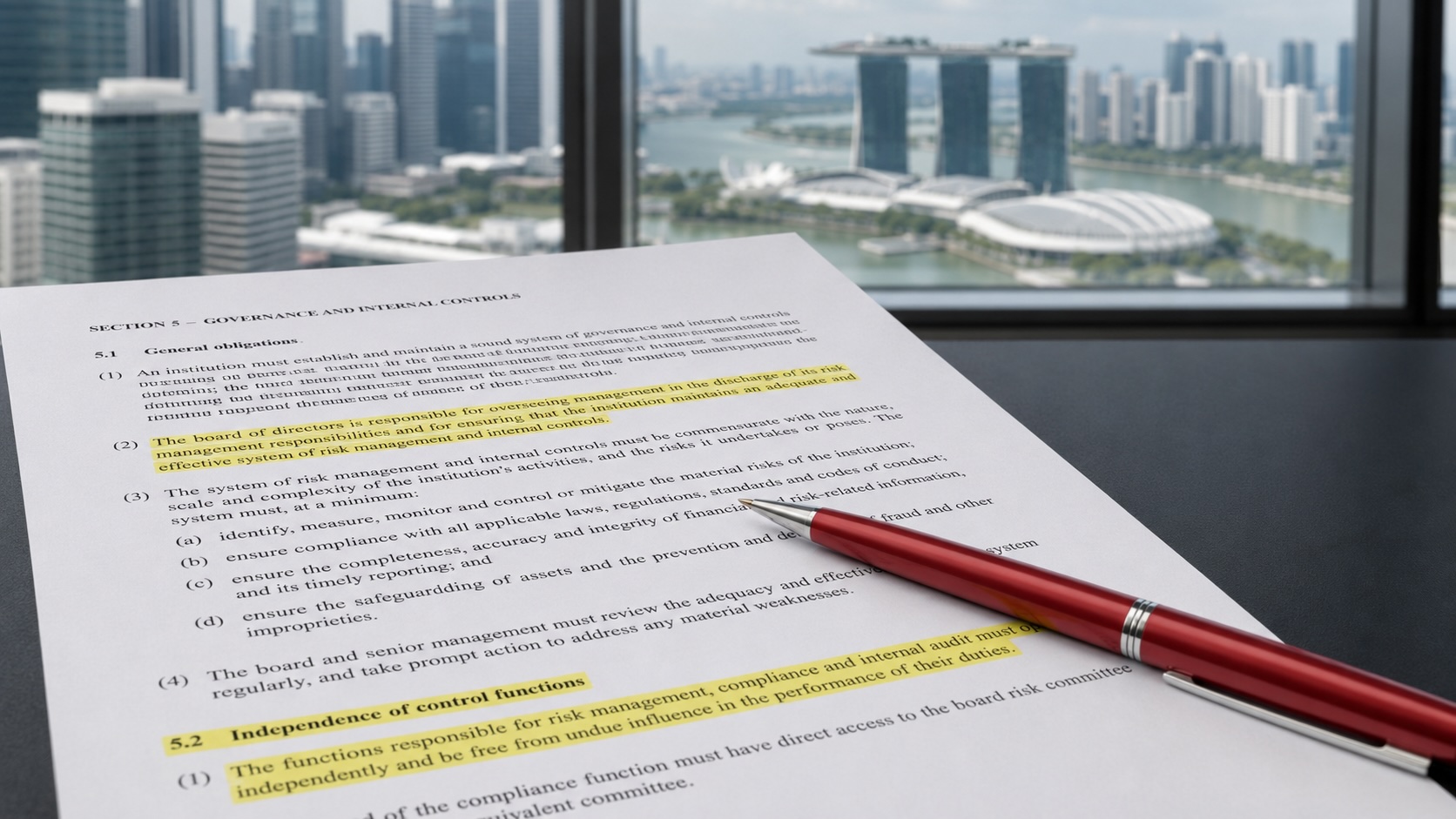

The Four CDD Phases — What Each One Is Actually Checking

MAS Notice 626 requires Customer Due Diligence with four mandatory components. Understanding what each phase is actually designed to detect — not just what documents it requires — tells you exactly where to focus your preparation and where gaps are most likely to stall an application.

For non-residents who also need corporate banking alongside personal wealth management, the nexus test and enhanced UBO requirements apply with added intensity. The guide on how the post-2023 compliance environment affects foreign companies seeking Singapore bank accounts maps the five pathways still available in 2026.

VerificationWhat it is checking for: whether the person presenting documents is who they claim to be, and whether the documents are genuine.

What flags non-residents specifically: expired documents within six months of application, names spelled differently across documents issued by different jurisdictions, identity documents from countries with documented forgery risk. Notarised or apostilled copies are required at most private banks. Video verification works for digital tiers but not for private banking activation — in-person identity verification by a bank-authorised officer is the standard.

What it is checking for: who actually owns and controls the assets and the account, behind any corporate or trust structures.

What flags non-residents specifically: offshore holding structures where the UBO trace is incomplete, trust arrangements where the beneficiary is discretionary rather than named, nominee shareholder arrangements without documented principals. Singapore banks trace ownership chains to individuals holding 25 percent or more. Complex layered structures are the most common cause of Phase 2 failure for international HNWI clients — simplification before engagement is consistently more efficient than documentation through layers.

What it is checking for: whether the stated purpose for the account is consistent with the client’s profile and whether the expected transaction patterns are plausible.

What flags non-residents specifically: stated purpose inconsistent with the client’s professional background, expected transaction volumes that materially exceed the wealth level documented, purposes that imply the account is a transit point rather than a wealth management vehicle. For private banking accounts, “investment management and long-term wealth preservation” is the standard accepted purpose. Descriptions that imply high operational transaction volumes without a clear business rationale create friction at Phase 3.

What it is checking for: the documented, verifiable origin of the assets the client intends to deposit and manage.

What flags non-residents specifically: this is where the majority of non-resident files stall. The verification standard is higher than most clients expect — not because Singapore regulators are unusually strict, but because the regulation explicitly requires verification, not acceptance. A self-declaration about wealth origin requires no documents to accept; verifying it requires evidence that traces assets to their source in a linear, contemporaneous chain. Every gap in that chain is a compliance flag, regardless of its innocent explanation.

Enhanced Customer Due Diligence: Three Triggers and Their Real Timeline Impact

MAS Notice 626 requires Enhanced CDD for three client categories. Each trigger has different practical implications for timeline, institution selection, and what additional documentation is needed.

| EDD trigger | What changes in practice | Realistic timeline impact |

|---|---|---|

| FATF-monitored jurisdiction | Senior management approval mandatory; independent verification of source of wealth beyond standard CDD; more intensive ongoing monitoring; some institutions decline outright | +4–8 weeks beyond standard CDD timeline |

| PEP or close PEP associate | Board-level approval at most institutions; detailed political exposure documentation; reviews every six months not annually; higher effective minimum at some banks | +4–12 weeks; subset of institutions decline PEPs entirely |

| Internal risk factors | Varies by factor: complex structures trigger UBO documentation cycle; high-risk business sector triggers industry-specific EDD; adverse media triggers investigation report | +2–16 weeks depending on complexity and factor type |

The PEP trigger is the one most frequently misunderstood. A Politically Exposed Person is not only a sitting politician. The definition covers anyone who holds or has held a prominent public function within the preceding twelve months — some institutions apply a two-year look-back. Senior executives of state-owned enterprises, members of international organisation governing bodies, military officers above a certain rank, and senior judicial officers all qualify. More importantly, immediate family members and known close associates are subject to the same Enhanced CDD regardless of their own activities.

I have seen clients genuinely surprised to learn that their business partner’s appointment to a state enterprise board made their existing banking relationship subject to retroactive ECDD. The bank did not change its behaviour — the client’s profile changed, and the bank’s continuous monitoring detected it. Notifying your relationship manager proactively when a PEP relationship is established, rather than waiting for the bank’s monitoring to discover it, is both a compliance obligation and a practical self-interest decision.

The Source-of-Wealth Verification Standard: What Compliance Officers Are Actually Trained to Look For

Phase 4 of CDD is where most non-resident files stall. Understanding what compliance officers are specifically trained to identify transforms an abstract documentation requirement into a concrete preparation checklist.

Officers are trained to verify four dimensions. First: plausibility — is the documented source of wealth consistent with the client’s professional and personal history? An individual in their late thirties claiming SGD 10 million from a career in mid-level management will receive scrutiny that an equivalent claim from an entrepreneur with a documented business exit does not. Second: contemporaneity — are the documents evidence created at the time of the wealth event, or retrospective reconstructions? A sale agreement from 2018 is contemporaneous evidence; a summary prepared by a lawyer in 2025 is not, standing alone. Third: scale consistency — does the wealth explained by the documented source match the quantum being deposited? Fourth: legal coherence — are the wealth events consistent with the legal and regulatory environment of the jurisdiction where they occurred?

Each of these dimensions generates a specific type of documentation gap that officers are trained to flag. Knowing the dimensions in advance means you can audit your own file before the bank does — and address gaps before they become compliance stall points.

The anti-tipping-off rule in practice: Under Section 48A of Singapore’s CDSA, it is a criminal offence for anyone who knows or suspects a Suspicious Activity Report has been filed to disclose this fact to the subject of the report. In practice: if a transaction is frozen and the bank provides only a generic “compliance review” explanation, an SAR may have been filed. The bank cannot lie about the existence of a hold, but it legally cannot tell you the reason. Engage a Singapore banking lawyer. Respond promptly and completely to all document requests. Do not interpret the silence as confirmation of the bank’s assessment of your situation — it is frequently a legal constraint rather than an indication of suspicion.

CRS and FATCA: The Tax Reporting Layer Running in Parallel

MAS Notice 626 governs AML and KYC. CRS and FATCA govern tax information exchange. They are separate frameworks running in parallel — and non-residents must satisfy both simultaneously, which creates a compliance surface larger than most clients expect when they first open a Singapore account.

Singapore has exchanged CRS information since 2018, with over 100 partner jurisdictions as of 2026. Singapore banks identify non-resident account holders, determine tax residency through a self-certification form, and report account balance, interest, dividends, and gross proceeds to MAS annually. MAS exchanges this automatically with the relevant home tax authorities. The account holder’s obligation within this system is the self-certification — a formal declaration of tax residency that must be updated within 90 days of any change.

The 90-day requirement catches more clients off-guard than any other ongoing obligation. A non-resident who moves from the UAE to Portugal, or takes up German tax residency alongside their existing Singapore residency, has 90 days to provide the bank with an updated self-certification reflecting the new position. Providing an outdated self-certification after a change in tax residency is a compliance breach that can result in account closure. For clients whose lifestyle involves spending time across multiple jurisdictions, maintaining a current and accurate self-certification is an active ongoing task, not a one-time document.

For US persons, FATCA adds a parallel reporting obligation: Singapore banks report US-person accounts to MAS under the US-Singapore Intergovernmental Agreement, which forwards the information to the IRS annually. Combined with FBAR and Form 8938 obligations in the United States, the dual compliance overhead is the primary reason most Singapore private banks have significantly reduced US-person acceptance since 2018. The non-resident tax compliance guide covers both CRS and FATCA in detail for clients banking in Singapore and Switzerland simultaneously.

The Pre-Application Compliance Checklist: What to Have Ready Before Bank Contact

The most effective compliance preparation happens before you make first contact with any bank. A complete pre-application file eliminates most of the additional information requests that extend timelines, and it signals to the compliance team that the client’s affairs are in the order required for a private banking relationship.

- Passport valid at least six months from application date; secondary ID also required

- Proof of address — utility bill, government letter, or bank statement within three months

- Tax identification number for every country of tax residency

- Completed tax residency self-certification — prepared in advance of the bank’s form

- Source-of-wealth chain — contemporaneous documents for every significant wealth event

- World-Check self-assessment — know your profile before the bank runs it

- PEP status confirmation — include family members and close business associates

- UBO structure chart if any corporate or trust structures are involved

- Bank reference letter from your primary existing institution

- If any adverse media exists: factual context letter prepared with legal input before application

- If resident in a FATF-monitored jurisdiction: independent notarised source-of-wealth verification

The proactive-transparency principle: The most effective ongoing compliance posture — after the account is open, not just during onboarding — is proactive transparency. Tell your bank about material changes before its monitoring detects them. A large incoming transfer pre-notified with documentation is a routine compliance event. The same transfer discovered through monitoring without client notification is a potential suspicious activity trigger. The content is identical. The compliance treatment is entirely different.

For the account opening process itself — including the six decision gates that determine whether an application succeeds — the guide to opening a Singapore bank account as a non-resident covers the full sequence. To check your likely compliance risk tier before approaching any institution, the client risk score calculator applies the same MAS-framework criteria Singapore banks use internally.

What Proactive Transparency Actually Looks Like in Practice

The proactive-transparency principle is easy to state and slightly harder to operationalise. Here is what it looks like in concrete terms across the three most common ongoing compliance scenarios for non-resident private banking clients.

Scenario one: you are about to receive a large wire transfer — the proceeds of a property sale in your home country, a business dividend, or the settlement of an inheritance. The amount is material relative to your account’s typical activity profile. The correct action: contact your relationship manager before the funds arrive, explain the source and the anticipated timing, and attach whatever documentation you have — the sale agreement, the dividend notice, the probate distribution. The compliance team will still review the transaction. But a pre-notified, documented inflow is a routine review, not an alert. The trigger threshold for suspicious activity monitoring is relative to your account’s established pattern; a transaction that exceeds that pattern without context is categorically different from one that arrives with it.

Scenario two: you change your country of tax residency. You move from Singapore to Germany, from the UAE to Portugal, from the UK to Switzerland. The 90-day self-certification update rule applies immediately. Do not wait for the bank to ask. Contact your RM, explain the change, and provide an updated tax residency self-certification. If you are now tax resident in multiple jurisdictions — which is common among internationally mobile clients — provide self-certifications for all of them. The documentation burden is modest. The compliance cost of the bank discovering an undisclosed change through its own monitoring is not.

Scenario three: a business associate, family member, or close professional contact is appointed to a senior position in a state-owned enterprise, a government body, or an international organisation. This may make them a Politically Exposed Person under MAS Notice 626’s definition — and it may make you a “close associate” of a PEP. Contact your RM proactively, explain the relationship, and allow the bank to assess whether enhanced due diligence applies retroactively to your relationship. This conversation is less comfortable than the others. But discovering it later, through monitoring or through a regulatory review, is structurally worse for everyone involved.

Managing Multiple Jurisdictions: Singapore Banking Alongside Swiss or European Accounts

Most non-resident HNWI clients who bank in Singapore also bank in at least one other jurisdiction — Switzerland, Luxembourg, the UK, or the UAE being the most common. Managing MAS Notice 626 compliance alongside the compliance obligations of those other jurisdictions is not inherently complicated, but it requires coordination that most clients leave to chance.

The key coordination point is CRS consistency. Under CRS, both your Singapore bank and your Swiss bank will report your account information to the same home tax authority. Those two reports need to be consistent with each other and with your tax declarations. An account balance reported to your home tax authority by your Singapore bank that does not match the balance declared in your home tax return is an automatic discrepancy flag in the tax authority’s system. It does not mean automatic audit — but it means your return receives additional attention that a consistent report would not generate.

The second coordination point is source-of-wealth consistency. If your Singapore bank’s compliance file shows wealth derived from a 2021 business sale and your Swiss bank’s file shows the same wealth as investment accumulation, a compliance officer conducting an EDD review with access to both files — which can happen in international regulatory cooperation contexts — has a factual inconsistency that requires explanation. Maintaining consistent source-of-wealth documentation across all banking relationships is not just good housekeeping; it is a practical risk management measure in a world where information exchange between jurisdictions continues to expand.

For non-residents managing compliance obligations across both Singapore and Swiss banking relationships, the non-resident tax compliance guide covers how AML, CRS, and FATCA obligations interact across both jurisdictions. For the account opening process at Singapore private banks, the six-gate guide covers what each institution actually evaluates before accepting a non-resident relationship.

MAS Compliance in the Context of a Broader Wealth Management Strategy

Non-resident clients who think of MAS Notice 626 compliance purely as a Singapore banking requirement miss something important: the compliance posture you establish at your Singapore bank feeds directly into your position at every other institution you bank with. This is because CRS information exchange means your Singapore bank’s annual report to MAS — which includes your account balance, tax residency, and income — is cross-referenced by your home tax authority against your Singapore bank’s reported figures and your home tax declaration simultaneously.

An inconsistency does not necessarily mean a problem. It means scrutiny. And scrutiny, in a well-managed multi-jurisdictional wealth structure, is perfectly manageable — provided the compliance posture at each institution is consistent and proactively maintained. The clients who face unexpected problems in CRS cross-referencing are almost never clients who have done anything illegal. They are clients who maintained their compliance obligations at each institution individually without coordinating across them, so small inconsistencies — in how source-of-wealth is described, in which tax residency is declared as primary, in how a joint account’s ownership is reported — accumulate into a pattern that requires explanation at precisely the moment when it is most inconvenient to provide one.

The practical solution is straightforward: maintain a master compliance file that records the source-of-wealth narrative, tax residency self-certifications, and account structures as reported to each banking institution, and review it annually for consistency across all jurisdictions. This is less burdensome than it sounds — for most clients, the relevant institutions are two to four banks across two or three jurisdictions, and the annual consistency review takes an afternoon with a qualified adviser who understands both the MAS Notice 626 framework and the equivalent frameworks in the other relevant jurisdictions.

For non-residents who bank in both Singapore and Switzerland — the most common multi-jurisdictional combination among HNWI clients who use Mamytova Consulting’s services — the non-resident tax compliance guide covers how the two frameworks interact and the specific consistency checks that prevent CRS cross-referencing surprises. For the account opening process itself, the six-gate guide to opening a Singapore account covers the practical steps from pre-application compliance self-assessment through to account activation.

Frequently Asked Questions

What is MAS Notice 626 and why does it matter for non-residents banking in Singapore?

MAS Notice 626 — Notice on Prevention of Money Laundering and Countering the Financing of Terrorism — is the Monetary Authority of Singapore’s primary AML and CFT regulation for licensed banks. It sets binding standards for customer due diligence, enhanced due diligence, ongoing transaction monitoring, and suspicious activity reporting. For non-residents, it determines how much documentation Singapore banks require at onboarding, how long the process takes, what triggers compliance reviews throughout the relationship, and under what circumstances a transaction can be frozen without explanation. The regulation was updated in 2024 with new provisions specifically addressing cross-border wire transfer patterns and non-resident relationship monitoring.

What source-of-wealth documents do Singapore banks require under MAS Notice 626?

Banks must verify source of wealth, not merely accept a declaration. For business-derived wealth: audited financial statements for at least three prior years, sale agreements or shareholder resolution documentation for the wealth realisation event, and bank statements showing receipt of the proceeds. For investment gains: brokerage statements covering the full accumulation period, tax returns confirming declared investment income, and custody transfer documentation from the originating institution. For inheritance: probate grant or equivalent, estate accounts, and asset transfer documents. For salaried wealth: employment contracts, payslips, and tax returns covering the accumulation period. Retrospective summaries prepared specifically for a bank application are not accepted as standalone source-of-wealth evidence.

What triggers Enhanced Customer Due Diligence (ECDD) in Singapore private banking?

MAS Notice 626 mandates ECDD for three categories: clients resident in FATF-monitored or higher-risk jurisdictions, Politically Exposed Persons and their immediate family members and close associates, and clients with specific internal risk factors — complex offshore structures, high-risk business sectors such as cash-intensive businesses or arms trading, unusual transaction patterns, or adverse media. ECDD requires senior management approval for account opening (not just relationship manager sign-off), more intensive source-of-wealth verification, and ongoing reviews every six months rather than the annual standard for non-ECDD relationships.

What is the Politically Exposed Person definition in Singapore banking?

Under MAS Notice 626, a Politically Exposed Person is any individual who holds or has held a prominent public function, typically within the preceding 12 months (some institutions apply a two-year look-back). The definition covers heads of state and government, senior politicians and government ministers, military officers above a specified rank, senior executives of state-owned enterprises, senior officials of international organisations, and members of judicial bodies in certain jurisdictions. Immediate family members — spouse, children, parents — and known close associates of PEPs are subject to the same enhanced due diligence requirements regardless of their own activities or roles. A PEP designation does not prevent account opening, but it triggers mandatory ECDD and narrows the pool of willing institutions.

Does Singapore participate in the Common Reporting Standard (CRS)?

Yes. Singapore has been a CRS participating jurisdiction since 2018 and exchanges account information with over 100 partner jurisdictions annually. Singapore banks are required to identify non-resident account holders, determine their tax residency through a self-certification form, and report account balance, interest income, dividend income, and gross proceeds from asset sales to the Monetary Authority of Singapore each year. MAS then exchanges this information with the relevant home tax authorities automatically. Non-residents must provide a tax identification number for every country where they are tax resident, and must update their self-certification within 90 days of any change in tax residency.

What is FATCA and does it affect Singapore bank accounts for US persons?

The Foreign Account Tax Compliance Act is US legislation that applies extraterritorially to all foreign financial institutions. Singapore has signed an Intergovernmental Agreement with the US implementing FATCA, requiring Singapore banks to identify US-person account holders and report their account details to MAS, which forwards the information to the IRS annually. US citizens and green card holders banking in Singapore face dual compliance obligations: the bank’s FATCA reporting on one side, and FBAR (FinCEN Form 114) and Form 8938 filing requirements in the US on the other. The combined compliance overhead is the primary reason most Singapore private banks have significantly reduced US-person acceptance since 2018.

Can a Singapore bank freeze my account without explaining why?

Yes, under Singapore’s anti-tipping-off provision in Section 48A of the Corruption, Drug Trafficking and Other Serious Crimes (Confiscation of Benefits) Act. If a bank suspects a transaction involves proceeds of a serious crime and files a Suspicious Transaction Report with Singapore’s Suspicious Transaction Reporting Office, it is a criminal offence for any person who knows the report has been filed to disclose that fact to the account holder. In practice, the bank provides a generic compliance review explanation and requests additional documentation. If a freeze extends beyond five business days without a clear resolution, engage a Singapore banking lawyer immediately. The bank cannot lie about the fact that a hold exists — only about the specific reason it cannot disclose.

How often will Singapore banks review a non-resident client’s compliance file?

Standard-risk non-resident clients are reviewed annually. Enhanced due diligence clients — PEPs, FATF-jurisdiction residents, clients with complex offshore structures — are reviewed every six months. Reviews are also triggered out-of-cycle by material changes: a new country of tax residency, a significant change in account transaction patterns, a change in UBO or corporate ownership structure, or new adverse media. Proactive notification to your relationship manager before a material change occurs prevents the bank from discovering the change through its own monitoring system — a discovery that is treated as an undisclosed event and triggers a more intensive review than a client-notified change does.

What is the 90-day tax residency self-certification rule in Singapore banking?

Under Singapore’s CRS implementing legislation, non-resident account holders are required to provide their Singapore bank with an updated tax residency self-certification within 90 days of any change in their country of tax residency. The self-certification is a formal declaration of the account holder’s current tax residency status, used by the bank to determine where to report the account under CRS. Providing an outdated or inaccurate self-certification after a change in residency is a compliance breach that can result in account closure. For internationally mobile clients who spend time across multiple jurisdictions, maintaining an accurate self-certification is an active ongoing obligation rather than a one-time document.

How is MAS Notice 626 different from FINMA AML requirements in Switzerland?

Both frameworks require customer due diligence, beneficial ownership verification, source-of-wealth documentation, and suspicious activity reporting. The key practical differences are in application and culture. FINMA requirements (primarily FINMA Circular 2011/01 and the Anti-Money Laundering Act) are applied with high precision and formality by Swiss banks; MAS Notice 626 is applied with a stronger emphasis on risk tiering and pragmatic assessment. Swiss banks tend to apply more rigid documentation standards regardless of risk tier; Singapore banks calibrate their requirements more explicitly to the client’s risk classification. For non-residents, the source-of-wealth standard is comparable across both jurisdictions — contemporaneous, evidenced, and chain-traced. The ECDD trigger thresholds and the anti-tipping-off provisions operate similarly in both jurisdictions.