Managing significant international wealth has never felt more complex than it does in 2025. Regulations tighten, geopolitical risks evolve overnight, and economic heavyweights shift the center of gravity for global capital. Consequently, high-net-worth individuals (HNWIs) and family offices cannot rely on yesterday’s playbook when selecting a primary financial hub. Three centers—Switzerland, Singapore, and Dubai (representing the wider UAE)—continue to dominate private-wealth conversations, yet each jurisdiction offers a very different blend of risk-management tools, tax advantages, and lifestyle benefits.

1. The High-Stakes Decision: Why 2025 Looks Different

Even though Switzerland’s alpine banks, Singapore’s glass-and-steel skyline, and Dubai’s desert megaprojects all symbolize enduring prosperity, the stakes rise each year. Geopolitical tremors now propagate faster through capital markets, and global transparency initiatives like the Automatic Exchange of Information (AEI) expose hidden weaknesses in legacy structures. As a result, choosing the wrong hub can erode returns, attract regulatory scrutiny, or restrict future flexibility.

Over the past decade, I have guided a diverse roster of clients—from tech founders in San Francisco to third-generation industrialists in Mumbai—through this very choice. I have watched motivations shift from pure tax savings to robust asset protection, from single-market access to multi-jurisdictional diversification. Therefore, instead of declaring a single winner, I aim to equip you with a granular, balanced comparison that reflects 2025’s realities.

2. Financial Powerhouse Metrics at a Glance

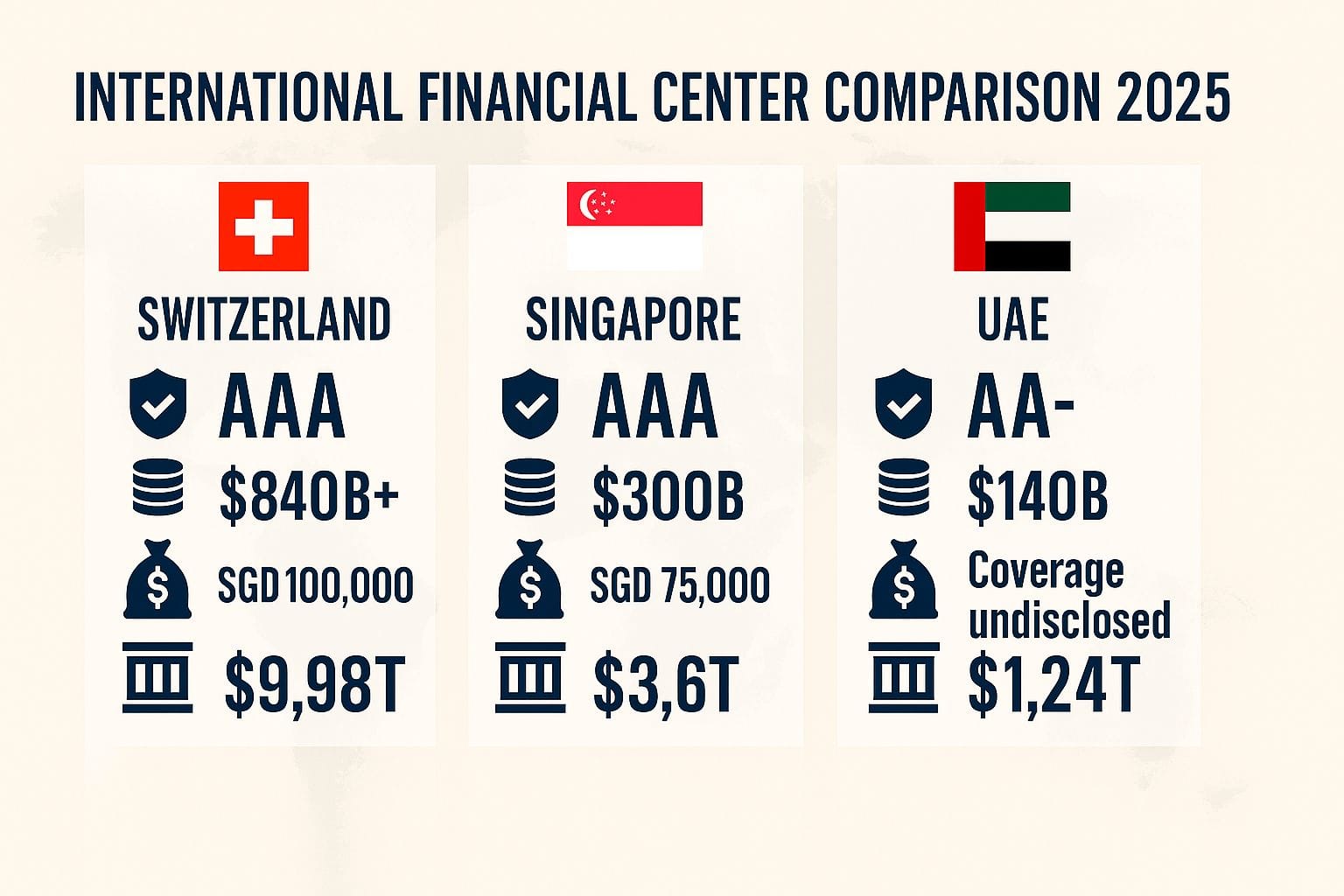

When clients first sit across the table, they usually ask, “Which center holds the most money?” or “Which government looks safest?” Numbers rarely tell the whole story; nevertheless, core metrics reveal how much firepower each jurisdiction can marshal during crises.

| Metric | 🇨🇭 Switzerland | 🇸🇬 Singapore | 🇦🇪 UAE |

|---|---|---|---|

| Credit Rating (S&P) | AAA | AAA | AA- |

| FX Reserves (USD, approx.) | $840 B+ (incl. gold) | $300 B+ | $140 B+ |

| Nominal GDP (2024 est.) | ~$940 B | ~$520 B | ~$540 B |

| Deposit Insurance | CHF 100,000 | SGD 75,000 | Framework exists¹ |

| Total Banking Assets (approx.) | ~$9.98 T² | ~$3.6 T³ | ~$1.24 T⁴ |

¹ The Emirates Deposit Insurance Corporation (EDIC) operates a coverage system, yet it does not publish standardized per-depositor limits.

² Swiss Banking Barometer 2024 / Swiss National Bank.

³ Monetary Authority of Singapore (MAS).

⁴ Central Bank of the UAE (CBUAE).

As you can see, Switzerland dwarfs its peers in sheer banking assets and FX reserves. Singapore impresses by maintaining AAA creditworthiness while managing assets equal to nearly seven times its GDP. Meanwhile, the UAE climbs quickly, underpinned by energy revenues and a strategy to diversify into finance, logistics, and tourism.

3. Why HNWIs Go Offshore in 2025

Before weighing pros and cons, clarify your deeper motivations. Once you rank these drivers, you can measure how each center satisfies them.

- Wealth Preservation – Safeguard capital in politically stable, strong-currency jurisdictions.

- Asset Diversification – Spread holdings across borders and asset classes to reduce concentration risk.

- Specialist Expertise – Access bankers, lawyers, and investment products unavailable at home.

- Enhanced Confidentiality – Maintain discretion within modern transparency rules.

- Tax Optimisation – Employ legitimate structures to minimise fiscal drag.

- Succession Planning – Establish cross-border trusts or foundations to transfer wealth smoothly.

- Business Gateway – Operate or invest globally from a strategically positioned hub.

Consequently, a tech entrepreneur selling a company might prioritise tax efficiency and digital-asset services, whereas an established family might focus on multi-generation trusts and geopolitical insulation.

4. Switzerland—The Established Bastion of Stability and Quality

Switzerland and private banking enjoy near-synonym status. Centuries of neutrality, direct democracy, and precision manufacturing have seeded a culture that values stability above all else. Clients nervous about currency debasement or political upheaval regularly gravitate to Swiss valleys, even in an age of full tax transparency.

4.1 Strengths I Consistently Observe

- Rock-Solid Political & Economic Stability. The Swiss franc trades as a safe-haven asset, and the state’s AAA rating plus $840 billion in reserves embody fiscal prudence.

- Unrivalled Banking Expertise. Swiss banks supervise close to $10 trillion in assets and excel at multigenerational wealth structuring, art financing, and physical precious-metal custody.

- Predictable, Pragmatic Regulation. The Financial Market Supervisory Authority (FINMA) enforces rigorous AML rules while the Federal Act on Data Protection (FADP) shields client data within clear legal parameters.

- Robust Asset-Protection Tools. Swiss foundations and properly structured trusts (where recognised) offer formidable protection against creditor or political risk.

4.2 Points to Consider

- Premium Pricing. Top-tier Swiss private banking demands high minimums and layered fees.

- Transparency Is the New Normal. Automatic Exchange of Information (AEI) rules mandate full disclosure to your home tax authority.

- Access Barriers. Smaller fortunes may rely on boutique private banks or independent external asset managers (EAMs).

4.3 Why Switzerland Often Stands Out

Whenever global markets wobble, I watch clients breathe easier knowing their core wealth sits beneath the Swiss regulatory umbrella. Although Swiss fees outstrip most competitors, many families consider the cost a premium for certainty and craftsmanship. When your top priority involves securing capital for your grandchildren rather than maximising this quarter’s return, Switzerland’s centuries-old ecosystem remains hard to beat.

5. Singapore—Dynamic Gateway to Asia and Innovation

While Switzerland perfected tradition, Singapore sprinted toward innovation. Over five decades, the city-state vaulted from regional port to global financial powerhouse, merging Western legal discipline with Asian dynamism. Its AAA rating confirms resilience, and its strategic location unlocks the world’s fastest-growing middle-class consumer base.

5.1 Strengths I Consistently Observe

- Economic Dynamism & Connectivity. Singapore’s Changi Airport and marine terminals maintain seamless links across Asia, making the city an ideal base for regional expansion.

- Investor-Friendly Tax Regime. Territorial taxation, zero capital-gains tax, and no inheritance tax attract entrepreneurs and fund managers.

- Cutting-Edge Banking & Fintech. Local heavyweights (DBS, OCBC, UOB) and global giants offer sophisticated digital platforms, while MAS pushes boundaries in green finance, blockchain pilots, and the Variable Capital Company (VCC) fund structure.

- Clear, Proactive Regulation. MAS ranks among the world’s most forward-thinking regulators, balancing innovation with robust AML enforcement.

5.2 Points to Consider

- Rising Cost of Living. Sustained success drives property and labour expenses sharply upward.

- Stringent On-Boarding. MAS expects detailed documentary evidence for source-of-wealth and source-of-funds, lengthening approval times.

- Regional Volatility. While Singapore itself remains stable, Southeast Asia’s geopolitical landscape demands ongoing attention.

5.3 My Take on Singapore

When a client needs frictionless access to Asian deal flow or values world-class digital infrastructure, Singapore often emerges as the frontrunner. Its tax advantages look especially compelling if you plan to establish residency, and its English-common-law foundation simplifies dispute resolution for international investors.

6. Dubai / UAE—Ambitious Hub Connecting East and West

Dubai, the UAE’s glittering metropolis, has mastered reinvention. Fuelled by petrodollars but no longer dependent on them, the Emirate positions itself as the zero-tax crossroads of Europe, Asia, and Africa. Although its AA- credit rating sits just below its peers, Dubai’s modern infrastructure and free-zone ecosystem keep capital flowing in.

6.1 Strengths I Consistently Observe

- Highly Attractive Tax Environment. Residents currently pay no personal income tax, capital-gains tax, or inheritance tax, while many free zones still offer 0 % corporate tax below taxable-income thresholds.

- Strategic Time-Zone & Connectivity. Flights from Dubai International Airport (DXB) reach 80 % of the global population within eight hours, enabling same-day business across continents.

- Business-Friendly Free Zones. DIFC (Dubai International Financial Centre) and ADGM (Abu Dhabi Global Market) operate under English common law, maintain independent courts, and permit 100 % foreign ownership.

- Cosmopolitan Lifestyle. Luxury real estate, world-class healthcare, and high-end retail attract globally mobile families.

6.2 Points to Consider

- Regulatory Maturity. Within DIFC and ADGM, regulators mirror international best practice, yet mainland frameworks still evolve.

- Regional Geopolitics. The Middle East’s complexities persist, although the UAE places a premium on security and diplomatic diversification.

- Depth of Traditional Private Banking. While the UAE’s wealth-management sector grows fast, it has yet to replicate Switzerland’s centuries of multigenerational expertise.

6.3 My Take on Dubai

Entrepreneurs who crave zero personal tax, seek proximity to emerging markets in Africa or South Asia, or value English-law arbitration often choose Dubai. However, I always advise clients to engage experienced counsel to navigate the nuanced interplay between free-zone and mainland regulations.

7. 2025 Showdown: Switzerland vs. Singapore vs. Dubai

After dozens of strategy sessions, clients still ask for a one-page scorecard. The following table distils each hub’s qualitative strengths and weaknesses, complementing the earlier numeric snapshot.

| Feature | 🇨🇭 Switzerland | 🇸🇬 Singapore | 🇦🇪 Dubai (UAE) |

|---|---|---|---|

| Political/Economic Stability | Exceptionally high (neutrality, CHF, AAA) | Very high (AAA, prudent policy) | High (AA-; stable domestically) |

| Regulatory Environment | FINMA—mature, strict, AEI compliant | MAS—mature, proactive, AEI compliant | DIFC/ADGM mature; mainland evolving, AEI compliant |

| Confidentiality/Privacy | Strong (FADP) | Strong (PDPA) | Good; improving |

| Private-Banking Depth | Unmatched (~$10 T AUM) | Very high (~$3.6 T AUM) | Growing rapidly (~$1.2 T AUM) |

| Niche Expertise | Precious metals, art, complex trusts | Asia markets, trade finance, fintech | Islamic finance, real estate, free-zone structuring |

| Personal Tax (Resident) | Moderate–high (cantonal variation) | Low–moderate (territorial) | Zero |

| Corporate Tax | Moderate (cantonal variation) | Competitive | 9 % federal / 0 % in many free zones |

| Ease of Doing Business | Good (efficient but formal) | Excellent (streamlined) | Excellent (especially in free zones) |

| Digital Banking & Fintech | Good; security focus | Leading edge | Rapid development |

| Geographic Focus | Europe & Americas | Asia & Oceania | MEASA corridor |

| Cost / Minimums | High | Moderate–high | Moderate |

| Lifestyle & Residency | Alpine privacy, natural beauty | Urban efficiency, multicultural | Cosmopolitan, tax-free living |

Transitioning from left to right, you notice a shift in emphasis from stability (Switzerland) to innovation (Singapore) to tax efficiency (Dubai). Consequently, no single center wins outright; instead, each one shines under different priorities.

8. Key Questions to Frame Your Decision

Whenever clients feel overwhelmed, I pivot to a structured questionnaire. Answer each prompt honestly; you will quickly see which jurisdiction aligns with your strategic objectives.

- What are my primary goals? Wealth preservation, market access, tax minimisation, business structuring, or succession?

- Which regions host my core business interests? Europe/Americas, Asia/Oceania, or MEASA?

- How much weight do I place on personal tax relief versus regulatory predictability?

- What banking sophistication do I need? Standard private banking or ultra-complex UHNWI solutions backed by trillions in AUM?

- How important is digital innovation and seamless fintech to my daily operations?

- Do I prefer well-established legal frameworks or feel comfortable with newer regimes?

- What compliance duties must I fulfil in my home country?

- Which lifestyle environment suits my family’s long-term plans—Alpine villages, hyper-efficient city living, or cosmopolitan desert luxury?

By ranking your answers, you turn an abstract comparison into concrete direction.

9. Implementation: Practical Next Steps

Making a jurisdictional move rarely ends with opening a bank account. You need a full implementation roadmap to translate strategic intent into tangible results.

- Engage Cross-Border Tax Counsel Early. Map out AEI reporting obligations and confirm treaty benefits.

- Perform Reputation Due Diligence. Screen counterparties, law firms, and banks to ensure alignment with your risk profile.

- Choose Governance Structures Wisely. Decide between trusts, foundations, family offices, or corporate wrappers based on succession goals and control preferences.

- Model Total Cost of Ownership. Account for setup fees, annual running costs, and hidden expenses (e.g., Swiss cantonal taxes or Singapore’s rising property rents).

- Confirm Residency Rules. Understand physical-presence requirements, substance tests, and potential exit taxes from your origin country.

- Plan an Exit Strategy. Regulatory landscapes shift; build flexibility to migrate structures if laws or personal situations evolve.

Moreover, allocate sufficient time—often six to twelve months—for licensing, banking approvals, and asset migration, especially in high-scrutiny environments like Singapore.

10. The Final Word: Crafting Enduring Wealth Strategies

In 2025, the line between local and global finance has effectively vanished. Capital travels at digital speed, regulators share data across borders, and families increasingly disperse across continents for education, health, and lifestyle. Switzerland, Singapore, and Dubai each answer this complexity with distinct value propositions:

- Switzerland delivers unparalleled stability, deep expertise, and a safety-first culture.

- Singapore offers forward-looking regulation, cutting-edge fintech, and privileged access to Asia’s growth engine.

- Dubai supplies zero personal tax, strategic connectivity, and free-zone flexibility tailored to entrepreneurs.

Ultimately, the best choice remains profoundly personal. Evaluate your risk tolerance, long-term goals, and family aspirations. Then, leverage specialised advisors who understand the intricacies of each jurisdiction to architect a structure that stands the test of time. Done correctly, your chosen hub will not merely store wealth; it will amplify opportunity, safeguard legacy, and empower the next generation to thrive in a relentlessly changing world.

Choosing by Client Profile: Which Centre Fits Whom

The academic comparison of Switzerland, Singapore, and the UAE across macro metrics is useful — but the decision for any individual client ultimately comes down to the match between their specific situation and each jurisdiction’s practical strengths. Below is a profile-based framework that reflects real onboarding patterns in 2026.

The European HNWI Seeking Stability and Discretion

Switzerland remains the natural primary banking jurisdiction for European high-net-worth individuals, particularly those from Germany, France, Italy, the UK, and Scandinavia. EU-resident clients benefit from the widest institutional access — mid-tier private banks start from CHF 500,000, and the full breadth of the Swiss private banking market opens at CHF 1 million. Geographic proximity enables in-person meetings with minimal disruption. The Swiss legal framework’s long-term stability and the depth of the local wealth management expertise are unmatched for clients with multigenerational wealth planning objectives.

For EU clients, Singapore or the UAE add value as secondary banking jurisdictions — providing Asian market access, currency diversification, or a domicile for business operating accounts in growth markets. Very few EU clients find it practical or necessary to replace Switzerland as their primary banking relationship.

The Asian or Middle Eastern Entrepreneur

For clients based in Southeast Asia, the Gulf Cooperation Council states, or South Asia, Singapore is often the logical primary banking jurisdiction. Geographic proximity, cultural familiarity with the region’s business practices, MAS’s understanding of Asian wealth sources, and Singapore’s role as a gateway to Asian capital markets all create a natural alignment. Singapore private banks are also more experienced in handling wealth derived from manufacturing, real estate development, and commodities in emerging Asian markets — source-of-wealth categories that can face greater scrutiny in Switzerland.

Switzerland, for this client profile, typically functions as the secondary or legacy jurisdiction — the ultra-long-term, ultra-conservative store of value holding generational wealth in segregated custody, while Singapore manages the more active investment and business banking needs.

The Internationally Mobile Business Owner

For entrepreneurs who are genuinely internationally mobile — spending time across three or more jurisdictions, operating businesses in multiple markets, with active transaction volumes — the Dubai model has become increasingly attractive since 2020. The combination of zero personal income tax, a rapidly improving private banking infrastructure, and the UAE’s position as a neutral hub between East and West creates genuine banking utility for this profile.

The critical caveat for UAE banking in 2026 is the FATF greylist removal: the UAE was removed from the FATF greylist in February 2024 following significant AML framework improvements, but Swiss and Singapore institutions continue to apply enhanced due diligence to UAE-sourced wealth as a standard practice. The reputational rehabilitation will take time, and clients banking primarily in the UAE should expect additional documentation requirements when establishing relationships in Switzerland or Singapore.

Practical Tax Considerations in 2026

One dimension of the comparison that deserves explicit treatment is the direct tax impact of banking in each jurisdiction — as distinct from the tax implications of residing in each country.

Swiss withholding tax (Verrechnungssteuer) applies at 35% to interest and dividend income paid by Swiss issuers to any account holder, including non-residents. For non-residents, this tax is generally fully or partially refundable under Switzerland’s extensive double taxation treaty network — but the refund process requires active administration and knowledge of the applicable treaty provisions. Clients who hold Swiss-issued securities in a Swiss account must factor this administrative layer into their total cost calculation.

Singapore imposes no withholding tax on interest income for non-residents and applies a 0% rate on capital gains for all account holders. Dividend income from Singapore-listed companies is taxed at the corporate level before distribution, so shareholders receive dividends from already-taxed profits. For investment-focused clients, this clean tax treatment on investment income is a genuine competitive advantage over Swiss account structures for non-EU residents who cannot easily reclaim Swiss withholding tax.

The UAE imposes no personal income tax, capital gains tax, or withholding tax. However, non-residents banking in the UAE who are tax resident elsewhere must still account for their UAE investment income and account balances under CRS in their home jurisdiction. The UAE’s tax neutrality at the banking level does not create tax neutrality for the account holder — a distinction that is frequently misunderstood.